International (EN)

International (EN) India (EN)

India (EN)

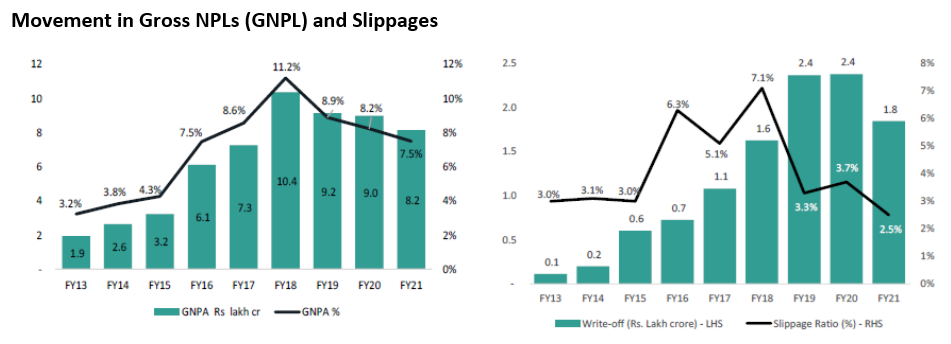

The Indian banking system had been witnessing a stark spike in Non-performing loans (NPLs) since 2018 when the corporate and wholesale banking book of banks witnessed a severe stress. However, post Insolvency and Bankruptcy Code, 2016 (IBC) and lower slippages in the corporate segment, wholesale NPL’s began to decline. Additionally, thanks to the continuation of the support and relief measures provided by the Reserve Bank of India (RBI) during the Covid pandemic, overall NPL’s have remained under control.

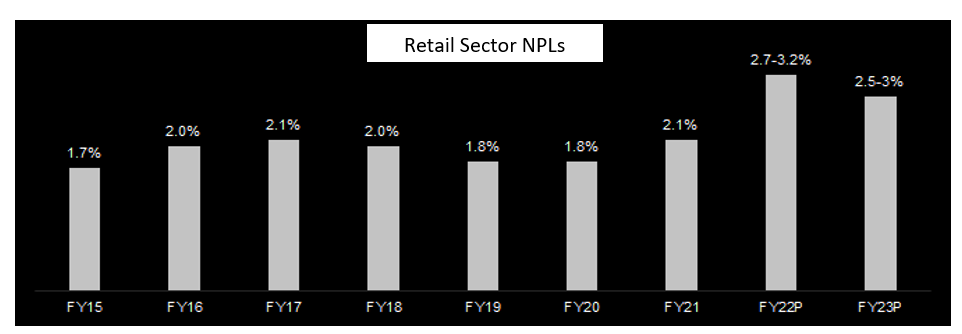

Going forward in FY22, India’s NPL is likely to be very different than that of 2018. In the past, NPLs came primarily from bigger, chunkier corporate accounts whereas, this time, smaller accounts, especially the MSME and retail segments, are expected to be more vulnerable. Overall, gross NPLs are expected to reach 8-9%, with an increase in retail sector NPLs and on gradual withdrawal of moratorium and relief measures.

While the overall NPAs in the banking system declined to 7.5% in FY21, the pandemic has resulted in one of the worst economic declines in decades. Moreover, NBFC bad loans are set to rise with RBI clarification on IRAC norms. At the back of these issues, the RBI announced a host of measures to enhance liquidity, ease the financial market conditions, address cash flow concerns, and improve the market sentiment.

Supportive Measures such as six-month debt moratorium, emergency credit line guarantee scheme (ECLGS) loans and restructuring provided relief to the borrowers and helped the customers who were financially impacted due to pandemic in rest of the fiscal 2021. These relief measures helped shield the asset quality deterioration.

Going forward in 2022, GNPA is expected to increase to 8-9%. Sectors such as airlines, hospitality, travel, gems and jewellery, auto dealers, and real estate are likely to be worst affected, given the discretionary nature of these sectors.

Retail Sector NPL Analysis

There has been a relative increase in retail NPLs and services (refer chart above). GNPL of retail loans was at 1.8% in fiscal 2020 rising to 2.1% in FY21 impacted due to Covid crisis. Unsecured segments such as personal loans and credit cards witnessed higher NPLs. However, complete impact of Covid fallout cannot be seen till now due to restructuring of loans.

Going forward, GNPL of retail loans is likely to increase to 2.7-3.2% in fiscal 2022 as the second wave impacts unsecured retail loans owing to loss in personal incomes and jobs. Even Micro, Small & Medium Enterprises (MSME) segments that had availed restructuring/ECLGS schemes are likely to face asset quality challenges, in the absence of withdrawal of moratorium. The only sigh of relief can be at the back of a solid economic growth, no or minor impact of third wave and no other major setback.

Credit Growth

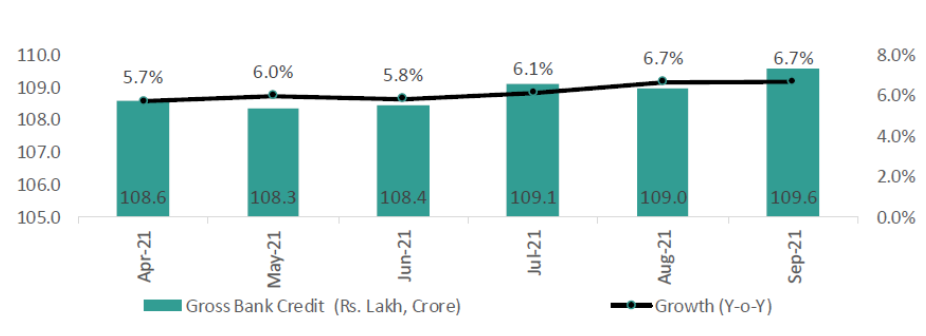

The non-food credit growth accelerated to 6.7% Year-on-Year (y-o-y) in September 2021 due to the easing of the lockdown restrictions and beginning of the festival season. The growth was driven mainly by the retail and industry segments, with services reporting sluggish growth. Under personal loans, housing and vehicle loans witnessed a strong growth at the back of strong demand during the festive season and easing of Covid related restrictions. As per CARE Ratings and media commentary, “property registrations in Mumbai recorded a rise of 35% y-o-y September 2021, while residential sales during January – September 2021 increased by 47% across the seven major cities in India. “

Continued improvement in the credit growth for the retail segment is anticipated due to the ongoing festival season, improving the confidence of the Indian consumers on account of the lower interest rate scenario in the Indian economy and a gradual opening of the Indian economy. However, any additional Covid waves could limit growth.

Way Forward

While Indian banks are plagued with high and bad debt, the country is still one of the leading players towards digitization. According to a recent joint study by IDC and Microsoft, “Digital transformation will add USD 154 billion to India’s GDP by 2021 and increase the country’s growth rate by 1% annually.” If this digital and artificial intelligence is used to control the NPA mess, Indian banks can come of the crisis much sooner than expected.

The Indian banking sector has been going disruption as well as innovation like never before. Powerful forces are transforming the overall retail as well as corporate banking industry. However, most of these strategies have been focused towards customer acquisition, portfolio augmentation and ease of doing business. The banking industry is yet to focus upon collection strategies and data analytics for controlling NPAs.

Banks face several challenges when collecting outstanding payments from delinquent customers. Developing a well-structured process, leveraging digitization, and upgradation of team resources and capabilities can maximize recoveries and prevent bad debts. With an increased focus on debt management, companies can reduce high costs and lost income and enhance customer focus, customer engagement, resilience, and profits.

Thus the need of the hour is not only a customer centric business model with optimal distribution but also a development of system that effectively manages capital, regulations and risks. For eg: scoring based early warning signal system, repayment forecasting models, digitization of collections and payment transactions, can help in reduction of distressed assets.