International (EN)

International (EN) India (EN)

India (EN)

Household debt has been building up in Asia for some time. According to an Asian Development Bank analysis, household debt in some Asian economies more than doubled from 2008 to 2021 .

The ADB explains that debt buildup is not necessarily a bad thing, and problems only arise when the pace is abnormal. An abnormal debt buildup exposes issuers to incompetent borrowers who contribute significantly to the issuers’ share of bad loans.

This scenario played out during the coronavirus pandemic, and the situation in Thailand offers the best illustration. About 1.2 million workers in Thailand fell out of jobs because of the pandemic. As part of the outcome, household debt among Thai workers expanded by 29.6%.

Such figures are bad news for debt issuers because it means they are likely to have more delinquents on their hands. So to recoup their losses, the issuers look up to debt collectors for help. But the collections process is challenging, especially when debtors feel threatened.

Unfortunately, most traditional debt collection techniques could easily breach fair debt collection regulations in many Asian countries. In Indonesia, for example, the Constitutional Court handed down a decision in 2020 that protects borrowers. Similar laws are in enforcement in India, Thailand, and many other Asian countries.

Digital debt collection is an apt alternative

To be sure, traditional debt collection techniques do work, only that they lead to many consumer complaints. This is true in Asia as in North America and other regions worldwide. A case in point is the 2019 Consumer Response Annual Report in which the US Consumer Financial Protection Bureau (CFPB) found that “debt collection was the second most complained about financial product or service in 2018.”

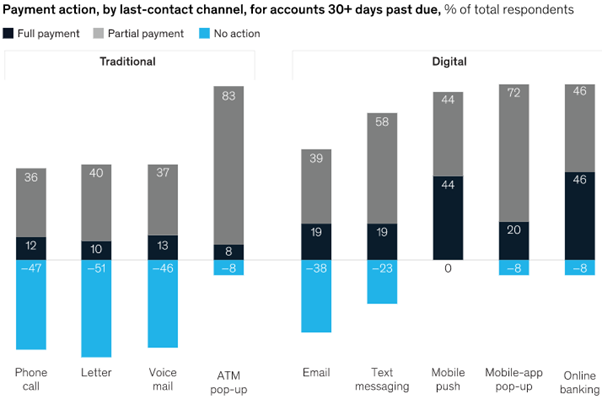

According to a 2019 McKinsey and Company survey, borrowers find the traditional contact channels, such as phone calls, letters, and voicemail, bothersome. This negatively impacts the engagement rates and, by extension, the payment actions. In fact, the survey established that borrowers are more likely to respond positively to digital contact channels than traditional – see the chart below.

Source: McKinsey

From the preceding, consumers are communicating that they prefer digital contact channels. But one wonders why this is the case?

Why digital debt collection matters and why the shift is inevitable

The most precise insight one can draw from the McKinsey survey, as illustrated above, is that digital-first collections are more effective. For example, contacting consumers by mobile push resulted in action.

Most importantly, the survey revealed that most consumers prefer to be contacted via digital channels, such as email and other digital-first avenues like SMS and social media.

The customers are not only digital-first but also digital-fast. They are constantly connected, and they know the immense potential of the technology in their hands. Specifically, the customers are accustomed to digital-focused customer experiences, and they demand the same from debt collectors.

In Asia, consumers favor organizations that offer compelling digital experiences. A great example is in digital commerce, where Southeastern Asia leads the world in transaction value. This trend is also feeding another revolution – non-cash payments. According to a recent report, non-cash payment transactions in the Asia Pacific (APAC) are snowballing and outpacing the rest of the world.

Thus, it is no longer a privilege but a necessity to implement digital-first techniques in the business. For example, in the case of debt collection, the methods enable companies to deliver an improved customer experience that increases consumer action and loan repayment.

Another reason the shift to digital debt collections is inevitable is customers’ demand for self-service and hyper-personalization. The digital age customers only offer their trust to businesses that they feel like they are empathetic. Thus, companies that engage with consumers through tailored communications and using preferred channels command substantial loyalty.

On the other hand, consumers prefer self-service because it translates to convenience. Specifically, most debtors want unguided processes delivered through digital platforms, typically the smartphone. Interestingly, some consumers want to avoid real-life conversations that might often be uncomfortable and, instead, follow automated and customer-centric processes.

Benefits of digital debt collection

1. Customer-centric collections approach eases anxiety:

We mentioned earlier that digital debt collection techniques put the consumer at the center of the action. For instance, hyper-personalized messaging communicates authenticity in the collector’s intention, which earns trust from the consumer.

Earning the trust and, consequently, loyalty is the ultimate goal of any brand. The emotional connection with the business removes all the conditions that might generate anxiety on the consumer’s part. Take the example of the Thai workers mentioned earlier. They fell out of jobs because of a global pandemic, and now they cannot honor their financial obligations. Naturally, the prospect of facing a debt collector under such circumstances could generate untold anxiety.

But if the consumers had a pre-existing personal relationship with the collectors (due to the use of digital debt collection techniques), there wouldn’t be room for anxiety. In particular, the borrowers know, from their relationship, that a workable solution is possible until the wind changes direction.

2. Improved recovery rates

In the McKinsey survey touched upon earlier, it was apparent that consumer action and payment rates improved when digital contact channels were used. Furthermore, McKinsey argues that digital debt collection techniques often generate better results because they’re backed by advanced analytics.

The strategies utilize robotic process automation (RPA) and artificial intelligence (AI) to strengthen their segmentation capabilities. This way, collectors can implement highly tailored contact strategies, leading to better customer outcomes and improved recovery rates for issuers.

3. Maintaining regulatory compliance

While the traditional collections approach still works, issuers are more likely to run afoul of regulations if heavily relied upon. We already saw that consumers complain a lot to regulators concerning debt collection when contacted via traditional channels.

Contrariwise, digital contact channels are designed to meet the requirements of debt collection regulations. Because issuers can easily segment and tailor communications, it is also easy to standardize the processes. For example, collectors can learn the best time to send an email alert to generate desired customer action.

Conclusion

The debt collection landscape, especially in the aftermath of the Covid-19 pandemic, is hostile to aggressive robocalls and agents. Unfortunately, chances of things reverting to the past are nil. The good thing is that issuers now have access to digital contact channels and strategies to increase customer engagement levels and, ultimately, improve recovery rates.

Going into 2022, issuers will focus more on segmentation and hyper-personalization of communication. Additionally, more collectors are likely to incorporate AI and RPA to improve customer outcomes.